The hardest technology problems now take longer to solve and more capital to commercialise than at any point in the venture era. The companies solving them are choosing to do it almost entirely out of public view.

Source: CNBC (24 yrs); Tracxn, via Alumni Ventures ($177B); S&P Capital IQ, via Apollo Academy (87%); Jay Ritter, via Adams Street Partners (12–14 yrs).

On June 12, 2026, SpaceX rang the opening bell at Nasdaq and completed the largest IPO in history, raising roughly $75 billion at a $1.77 trillion valuation, twenty-four years after Elon Musk founded the company in a warehouse in El Segundo.

For almost the entirety of its life, SpaceX built rockets, launched satellites, and eventually merged with an AI lab, entirely outside public markets. By the time ordinary investors could finally buy a share, the company had already built Starlink into a global network, flown astronauts, and become one of the most valuable enterprises on Earth. Retail investors weren't there for the breakthrough. They arrived for the valuation.

That is no longer an outlier story. It is becoming the default path for deep tech: the companies working on semiconductors, biotechnology, fusion, robotics, aerospace, and frontier AI. Within weeks of SpaceX's debut, both Anthropic and OpenAI confidentially filed their own IPO paperwork, having reached private valuations near $965 billion and $852 billion respectively without ever trading a public share. Three of the most consequential technology companies of the decade all chose to spend their most important years entirely in private hands. This piece looks at why that's happening, what it actually costs in capital and time to commercialise deep tech, and what it means for anyone trying to get investment exposure to the industries that will define the next decade.

Why deep-tech founders are choosing to stay private

Here are the five reasons the most ambitious technical teams are delaying, or entirely avoiding, public markets for as long as they can:

- Patience over pressure. A real scientific or engineering breakthrough rarely arrives with an obvious business model attached. Public markets expect quarterly proof of monetisation; deep tech often needs years to find the right one. Staying private buys the runway to get the model right before being forced to defend one every ninety days.

- Control over consensus. Private ownership means no earnings calls, no activist shareholders, and no stock-price reaction to a single delayed launch. Founders can make ten-year bets on unproven physics or biology without answering to a market with a ninety-day memory: a freedom public boards rarely extend.

- Focus over filing. Preparing for an IPO consumes enormous leadership bandwidth: audited multi-year financials, governance overhauls, disclosure controls, roadshows. Teams solving hard science problems would rather spend that time on the technology, especially when private capital is abundant enough that the listing isn't needed to fund growth.

- Substance over sentiment. A decade of thinly profitable tech listings trained retail investors to read an IPO as the moment insiders cash out, not the moment a company begins its next chapter. Companies with genuine technology increasingly wait until growth and profitability make that reading impossible before they ring the bell.

- Ownership over dilution. If a company can raise hundreds of millions privately at a compelling valuation without ceding board seats to public shareholders, there's little reason to divide the pie sooner than necessary. Founders confident in their trajectory keep control and equity for as long as private markets will let them.

The rise of private capital

Global assets under management held in private markets, 2000–2024

Source: Preqin. 2000 and 2007 reflect global private-equity AUM (Preqin, cited in Preqin's Q3 2012 report); 2010–2022 reflect total private markets AUM, comprising private equity, real estate, infrastructure, private debt and natural resources (Preqin, via The Investment Association, 2024); 2024 reflects total private markets AUM (McKinsey Global Private Markets Review 2024, via Adams Street Partners). The 2007-to-2010 step reflects a broadening of scope as much as underlying growth.

The capital and time it actually takes to commercialise a breakthrough

Deep tech isn't slow because founders lack urgency. It's slow because physics, biology, and regulation don't compress on a venture fund's schedule. A software startup can ship, learn, and iterate in weeks. A company built around a new drug, a new chip node, or a new energy source is often years away from its first real signal of product-market fit, and the capital required to get there scales accordingly.

Sources: Tufts CSDD and RAND (biotech); Construction Physics (semiconductors); Waveup and DCVC (fusion energy); TechCrunch (defense tech). Figures are representative midpoints, not precise averages.

Time and capital required to reach commercial scale

Representative figures by category. Bubble size reflects typical capital intensity

Sources: Tufts CSDD and RAND (biotech); Construction Physics (semiconductors); Waveup and DCVC deep-tech reporting (fusion, defense); TechCrunch (Anduril). Figures are representative midpoints, not precise averages.

This is why deep-tech investing behaves more like patient infrastructure or private-equity investing than classic software venture capital. Specialist deep-tech funds report typical 7–10-year holding periods before a first meaningful return, and BCG's research finds that, over the same period, deep-tech-focused funds delivered an average IRR of roughly 25%, statistically similar to the 26% posted by traditional VC funds: evidence that deep tech's added complexity hasn't required investors to accept lower returns.

The deep-tech journey: from pre-seed to the surface

An IPO isn't a fundraising event that a company can schedule whenever it wants liquidity. It's a checkpoint that only becomes available once a specific set of milestones has been cleared: audited financials, governance built for public scrutiny, and growth investors who can underwrite for years, not quarters. Here's what that journey typically looks like for a deep-tech company, from the first prototype to "the surface."

The aging IPO

Median age of a company at the time it goes public

Source: composite of Jay Ritter (University of Florida) IPO statistics, Renaissance Capital, and Nasdaq Economic Research, 2026. SpaceX shown separately as an individual case (CNBC), not part of the trend average.

What this means for investors seeking exposure to emerging industries

Here are three implications for allocators:

- A longer timeline. If the median deep-tech company now spends 12 to 14 years private, and category leaders like SpaceX spend more than twice that, exposure to this growth means committing capital for a decade or longer, not a typical three-to-five-year holding period. Some venture firms are already extending fund lifecycles beyond ten years to match.

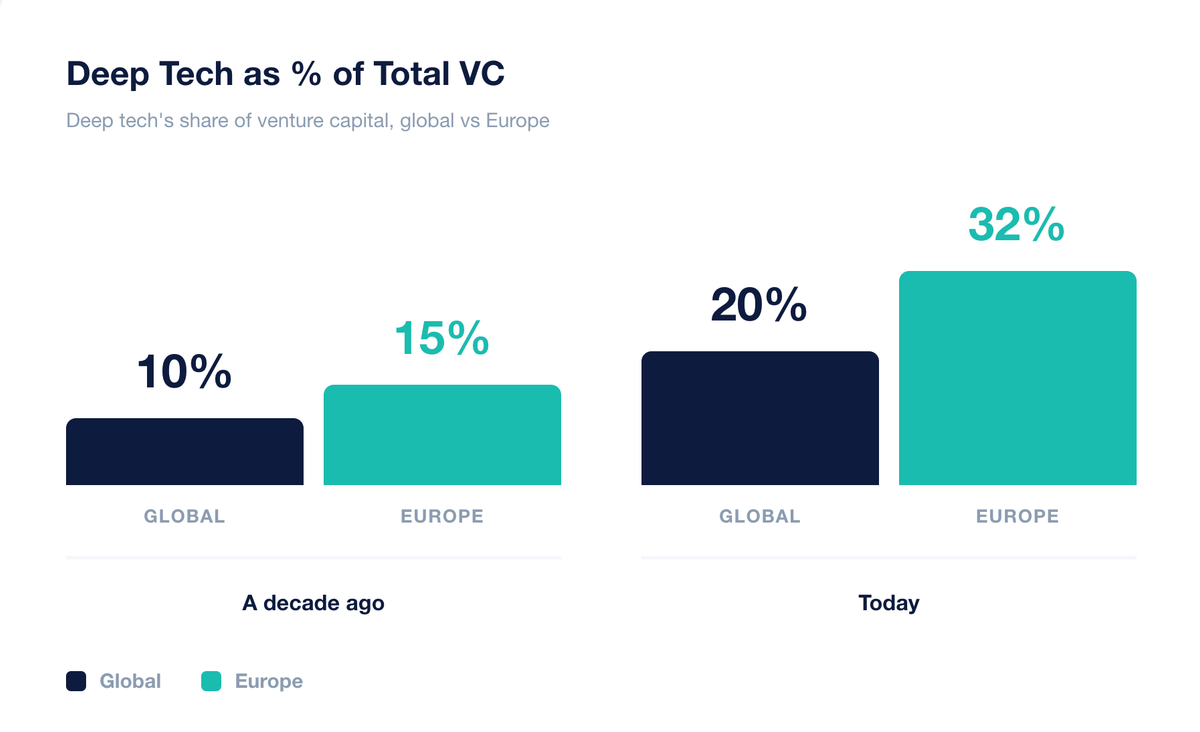

- Public portfolios quietly miss the sector. Deep tech now takes roughly 20% of global venture capital, double its share a decade ago, and in Europe that figure has climbed to roughly a third of all tech investment. Almost none of that value is visible to an investor confined to public indices. The number of publicly listed U.S. companies has already fallen by close to half since the late 1990s. An investor who only buys what's on an exchange isn't underweight deep tech; they're largely absent from it until the very end of the story.

- Lenders still favour what they can see. Traditional bank lending is built around collateral such as real estate, equipment, and inventory: assets a bank can repossess and value with confidence. A deep-tech balance sheet is dominated by unproven prototypes, years of R&D, and intellectual property that's hard to price outside the company itself. That mismatch is structural, not temporary, and it's a core reason deep tech leans so heavily on equity-based private capital (venture, growth equity, sovereign wealth, family offices) rather than debt.

Deep tech's growing share of venture capital

Percentage of total venture capital allocated to deep-tech companies

Global figures: BCG, “An Investor's Guide to Deep Tech”. Europe figure is illustrative, consistent with McKinsey's finding that deep tech reached roughly a third of European venture capital by 2024 (October 2025 report, via Alumni Ventures).

The AI wave now testing public markets makes the same point from a different angle. Anthropic and OpenAI both confidentially filed for IPOs in 2026, arriving at the door of the public markets only after reaching private valuations near $965 billion and $852 billion. Whatever the eventual outcome of those listings, the pattern holds: by the time an emerging-industry leader is available to a public-market investor, most of its value has typically already been created privately.

Key takeaways for allocators

- Deep tech's growth is increasingly happening off the public map. Meaningful exposure now requires venture, growth-equity, or private-credit relationships, not just a brokerage account.

- Time horizon matters more than ever. Underwrite deep-tech exposure on a 7–10+ year basis, in line with how the specialist funds themselves invest.

- An IPO is a milestone, not a starting gun. By the time a deep-tech company lists, the technology risk is usually resolved. What's left to price is growth and execution.

- Illiquidity is the toll for early access. Secondaries and pre-IPO platforms can shorten the holding period, but rarely eliminate the wait entirely

NonPublic Pty Ltd (ABN 49 607 216 928) holds Australian Financial Services Licence #482668. Investments are available to wholesale and sophisticated investors as defined under the Corporations Act 2001. This content is general in nature and does not constitute financial product advice. It does not take into account your objectives, financial situation, or needs. Investing in private markets involves significant risk, including the potential loss of your entire investment. Past performance is not a reliable indicator of future results. You should obtain independent financial advice before making any investment decision.

The Pre-IPO & Private Investment Marketplace for Australian Wholesale Investors

Get started today to learn how NonPublic can give you access to exclusive deals.

Get Started